Gen Z consumers are driving the credit industry rebound, TransUnion report finds

The youngest generation of consumers are leading the way in new credit originations, according to TransUnion. Here's how to choose the right credit card company and build better spending habits. (iStock)

Originations for credit cards, home loans and other financial products took a hit during the COVID-19 pandemic as consumers tightened their budgets and were more conservative with their spending. About two years into the global health crisis, demand for credit has nearly doubled — and it's been driven by Gen Z consumers, according to a new report from TransUnion.

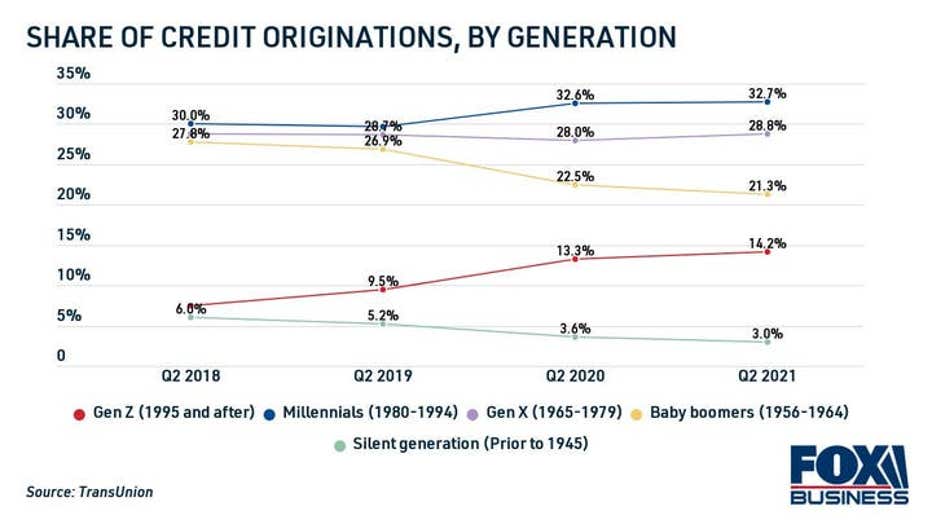

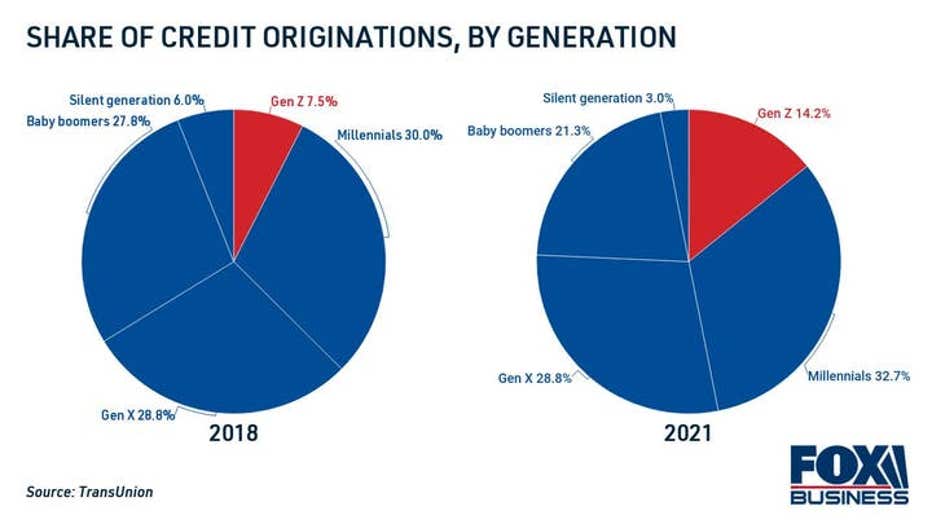

Between Q1 2020 and Q2 2021, new credit originations increased from 8.6 million to a record 19.3 million, the report found. While millennials still lead the way with the largest share of originations, the youngest generation of Americans is taking out credit at a rapidly growing rate.

Much of this generational growth follows the natural trajectory for when consumers need financial products throughout different stages of their lives, according to TransUnion senior vice president, Matt Komos.

"From a generation perspective, consumers tend to follow a pattern of credit needs as they go through life events," Komos said.

This includes taking out a credit card during college, buying a car and even borrowing a home loan — financial milestones that are common for consumers in the 18-26 age range.

HOW TO FIND THE BEST TRAVEL REWARDS CREDIT CARDS

Plus, Gen Z consumers have been more confident in their ability to borrow money due to positive economic conditions while they were coming of age. Because of this, Gen Z "bounced back pretty quickly" when it comes to post-pandemic financial recovery, Komos said.

Access to online financial tools has also been instrumental in helping digital-native Gen Z consumers thrive during this period. They're able to check their credit scores, compare interest rates for financial products and even see their estimated payoff terms with loan calculators, all from their smartphones.

"It’s transformational in terms of how consumers engage with and understand credit," Komos said. "Overall, it’s great for the credit ecosystem."

In addition to taking out new financial products, Gen Z consumers are also growing their credit balances. The average balance per Gen Z cardholder grew 13.9% year-over-year, compared to 1.8% for millennials.

Growing credit balances can be damaging since any credit card balance carried over from month to month will be charged interest. The good news is that serious delinquency rates among Gen Z declined from 2.31% in Q3 2019 to 1.52% in Q3 2021.

As the youngest generation of consumers demands access to financial products, it's important for Gen Z consumers to research the best credit options for their needs, including credit cards. If you're considering opening a new credit card account, be sure to compare terms across multiple issuers to find the best credit card offer for your needs. You can view interest rates, rewards programs and sign-up bonuses for free on Credible.

CAPITAL ONE INTRODUCES NEW STUDENT REWARDS CREDIT CARDS

How to choose a credit card

With so many credit cards on the market, it can seem like a challenge to find the one that will be most beneficial for your financial goals. Follow these steps to choose the best credit card for your unique needs:

- Check your credit score. The higher your credit score, the better your chances are of being approved for a card with favorable terms like a high borrowing limit and a low interest rate. If you have a less-established credit report, consider taking out a secured credit card with a security deposit to build your score.

- Identify your financial goals. There are plenty of different types of credit cards, from cashback cards to help you earn up to 5% back on everyday purchases to travel rewards cards that accumulate airline miles you can use toward flights and hotels. You can also utilize a balance-transfer card that helps you save money on interest with a 0% introductory APR offer.

- Consider the terms. Credit card interest rates vary widely depending on your credit history, the credit card issuer and the type of card you need. You should also consider annual fees, late payment fees, balance transfer fees and foreign transaction fees. The card's annual percentage rate (APR) will give you the most accurate picture of the cost of credit.

HOW DO BALANCE TRANSFERS AFFECT YOUR CREDIT SCORE?

Keep in mind that taking out a credit card will require a hard credit check, which will temporarily lower your credit score. Additionally, the number of credit cards you have and the average credit age on your account will impact your overall score.

But there's good news: since opening a new card will give you access to a new line of credit, it will raise your overall credit limit and lower your credit utilization ratio. This can improve your credit score, but be wary to keep your spending in check. You should pay off your credit card statement balance in full each month to avoid paying interest.

You can compare all types of credit cards, from rewards cards to balance-transfer credit cards, on Credible's online marketplace. Doing so will not impact your credit score.

WHAT TO DO IF YOU CAN'T MAKE THE MINIMUM PAYMENT ON YOUR CREDIT CARDS

Tip: Get existing credit card debt under control

Credit cards offer perks that are unmatched by other financial products, but those rewards can come at a high price if you're paying interest. The average interest rate on credit cards assessed interest was 17.13% in August 2021 according to the Federal Reserve, which is near all-time highs.

If you can't keep up with ever-growing credit balances, consider consolidating your credit card debt into a personal loan. These are lump-sum loans that you repay with a fixed interest rate and loan term, so your monthly payments will stay the same. In contrast with credit cards, personal loans offer a more predictable debt payoff schedule.

More importantly, a personal loan may be able to save you money over time with lower interest rates. The average rate on a two-year personal loan is 9.39%, per Fed data. By paying off your credit card debt at a low, fixed rate, you may be able to reduce your monthly payments and save thousands in interest.

A recent Credible study found that credit card users have the potential to save nearly $2,400 and lower their monthly payments by $66 by consolidating debt with a personal loan.

See your estimated personal loan rate without impacting your credit score on Credible. Then, use a personal loan calculator to estimate your monthly payments and total interest costs.

HAVE BAD CREDIT? HERE'S WHAT YOU CAN DO TO HELP FIX IT

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.