Graduates can save more money than ever as fixed student loan refinance rates set record low

Fixed student loan refinance rates set a new record low during the week of Dec. 13, which means that borrowers have the opportunity to reduce their monthly payments, pay off their loans faster and save more money on their college debt. (iStock)

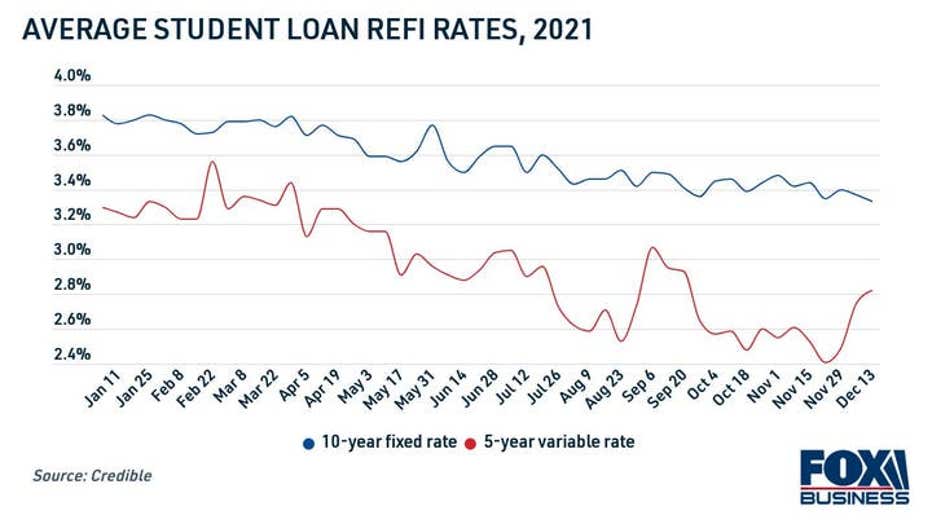

Fixed student loan refinance rates have fallen to a new record low, giving borrowers the opportunity to save more money on their student debt than ever before.

Interest rates on 10-year fixed-rate refinance loans averaged 3.33% for the week of Dec. 13, according to Credible. This is the lowest fixed student loan rates have been since Credible started collecting this data in June 2020.

STUDENT LOAN DEFERMENT EXTENSION: WHAT BORROWERS SHOULD KNOW

Variable interest rates for the 5-year refinancing term rose significantly during the same week, to 2.82%. Still, the variable rate is much lower than it was during the same time last year, when they were 3.20% on average.

With student loan refinance rates at historic lows, student loan borrowers have the opportunity to reduce their monthly payments, pay off their debt faster and save money on total borrowing costs over the life of the loan.

Keep reading to learn more about refinancing to a private student loan. Browse student loan refinance rates from private lenders in the table below, and visit Credible to see refinancing offers tailored to you without impacting your credit score.

WHAT IS A GOOD ANNUAL PERCENTAGE RATE (APR) ON A PERSONAL LOAN?

How to qualify for student loan refinancing

Student loan refinancing is when you take out a new loan to repay your current student debt with better terms, such as a lower interest rate. There are many private student loan lenders that offer refinancing, and the process can be done completely online.

When you refinance your student loan debt, your loan amount will stay the same, but your other terms will likely change. It may also be possible to move all of your loans into one monthly payment with student loan consolidation. You can choose a shorter loan term to pay off your student debt faster, or you can opt for a longer-term loan to lower your monthly payments.

Private student loan lenders determine your interest rate based on a number of eligibility criteria, including:

- Responsible financial history. Borrowers with a good credit score and low debt-to-income ratio will have the best chance at qualifying for student loan refinancing at a low interest rate. Borrowers with bad credit could consider enlisting the help of a creditworthy cosigner to qualify for student loan refinancing.

- Loan repayment terms. Larger loans may come with higher interest rates — plus, you'll be paying more in interest over time since it's assessed on a larger amount. Shorter loans will typically offer lower interest rates, while longer loan terms will cost more to borrow over time.

- Type of interest rate. Fixed-rate loans tend to come with higher rates, since borrowers can lock in their rate for the entirety of the loan term. Variable-rate loans tend to offer lower rates, which may rise or fall over the life of the loan depending on market conditions.

You can compare student loan rates on Credible for free with a soft credit pull, then use a student loan calculator to determine how much you can save by refinancing.

HOW TO CHECK YOUR FULL CREDIT REPORT WITHOUT A HARD CREDIT PULL

Should you refinance federal student loans?

Refinancing may help some borrowers lock in a lower rate on their college debt, but there are a few things federal student loan borrowers should know before switching to a private loan.

Interest rates are set differently. Federal student loan rates are fixed across all borrowers depending on when the loan was originated, whereas private student loan interest rates vary by lender depending on a borrower's creditworthiness. Plus, private lenders tend to offer rate discounts, such as an interest rate reduction for setting up automatic payments (sometimes called an Autopay discount).

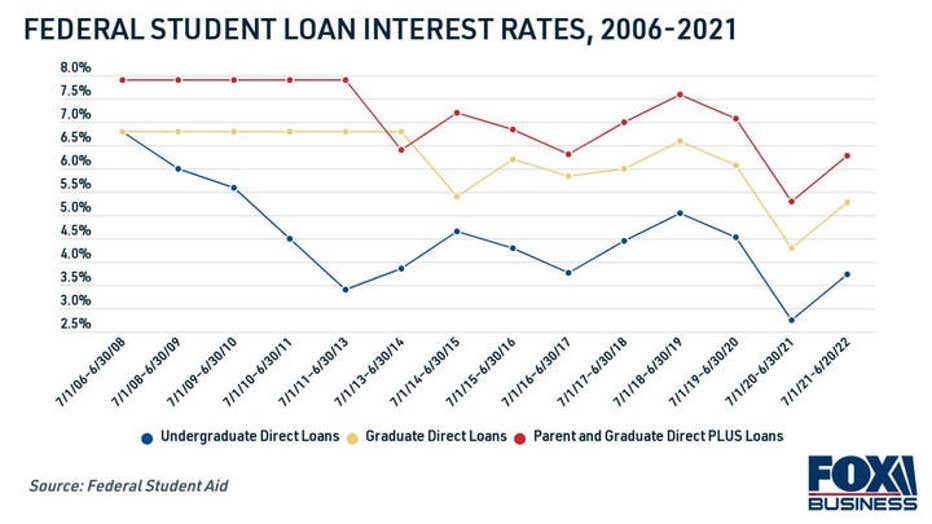

Borrowers with a high credit score and a low debt-to-income ratio may qualify for a lower interest rate through a private lender, but it depends on the fixed federal student loan rate when the loan was disbursed. Here are the current federal student loan interest rates for loans disbursed between July 1, 2021, and June 30, 2022:

- Undergraduate Direct Loans: 3.73%

- Graduate Direct Loans: 5.28%

- Parent and Graduate Direct PLUS Loans: 6.28%

WHAT IS THE MINIMUM CREDIT SCORE NEEDED TO GET A STUDENT LOAN?

Private student loan lenders don't charge refinancing fees. When you borrowed your federal loan, you likely had to pay a one-time loan fee that was a portion of the total loan amount. Federal Direct Loans disbursed on or after Oct. 1, 2020 were assessed a loan fee of 1.057%. Direct PLUS loans disbursed during the same time period have a loan fee of 4.228%

Private student loans aren't eligible for federal benefits. By refinancing to a private student loan, federal student loan borrowers are waiving several federal loan protections like income-driven repayment plans, administrative forbearance and select student loan forgiveness programs. Federal student loan payments are currently paused through May 1, 2022, which means that refinancing your federal loans into a private loan now would mean you have to resume monthly payments upon approval.

Still, it might be wise to lock in a private student loan refinance rate while rates are at record lows. Visit Credible to see your student loan refinancing offers, so you can determine if it's worth it to refinance your federal student loan debt.

PERSONAL LOAN ORIGINATION FEES: ARE THEY WORTH THE COST?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.